During our recent meeting with TAH, it was raised with us that investors need to consider Lotteries as an infrastructure asset. Without doubt the highly attractive Lotteries business is currently being overshadowed by the problems in Wagering and Gaming Services (which is now a non-core asset and likely to be divested at earliest opportunity). Post this meeting we have conducted the exercise of valuing the Lotteries business like an infrastructure asset. Our assumptions and valuation are presented below.

Lotteries – is it an infrastructure asset? Management believes the lottery business should almost be viewed like a infrastructure asset given the business has infra-like characteristics –

(1) periodic price increases (approximately at inflation like growth);

(2) monopoly like market position in most Australian states given unique long-dated licenses;

(3) strong support from the government (state governments are very dependent on the revenue they get from lotteries, however, risk remains that governments start demanding an increase to royalties but management hasn’t experienced that as of now); and

(4) mostly recession proof (lottery sales are not highly sensitive to the macro conditions, is habitual to most people and hold up pretty well in downturns given sentiment towards winning money to remain financially stable).

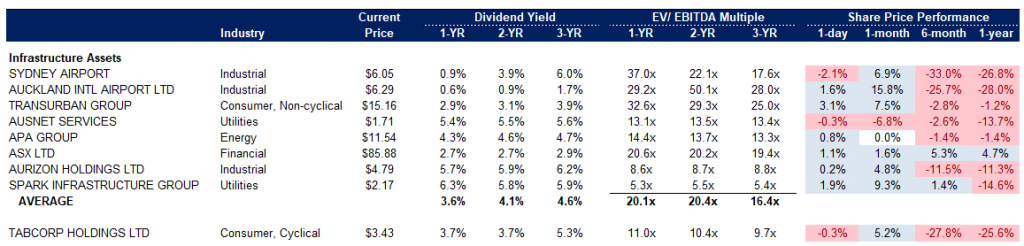

ASX Infrastructure peer group. In the table below we have provided the breakdown of the peer group we used in this exercise. SYD and TCL (and AIA) tend to skew the overall peer group average.

In any case, given the valuation multiples of this peer group (and what TAH is currently trading on), you can appreciate why management is keen to highlight this.

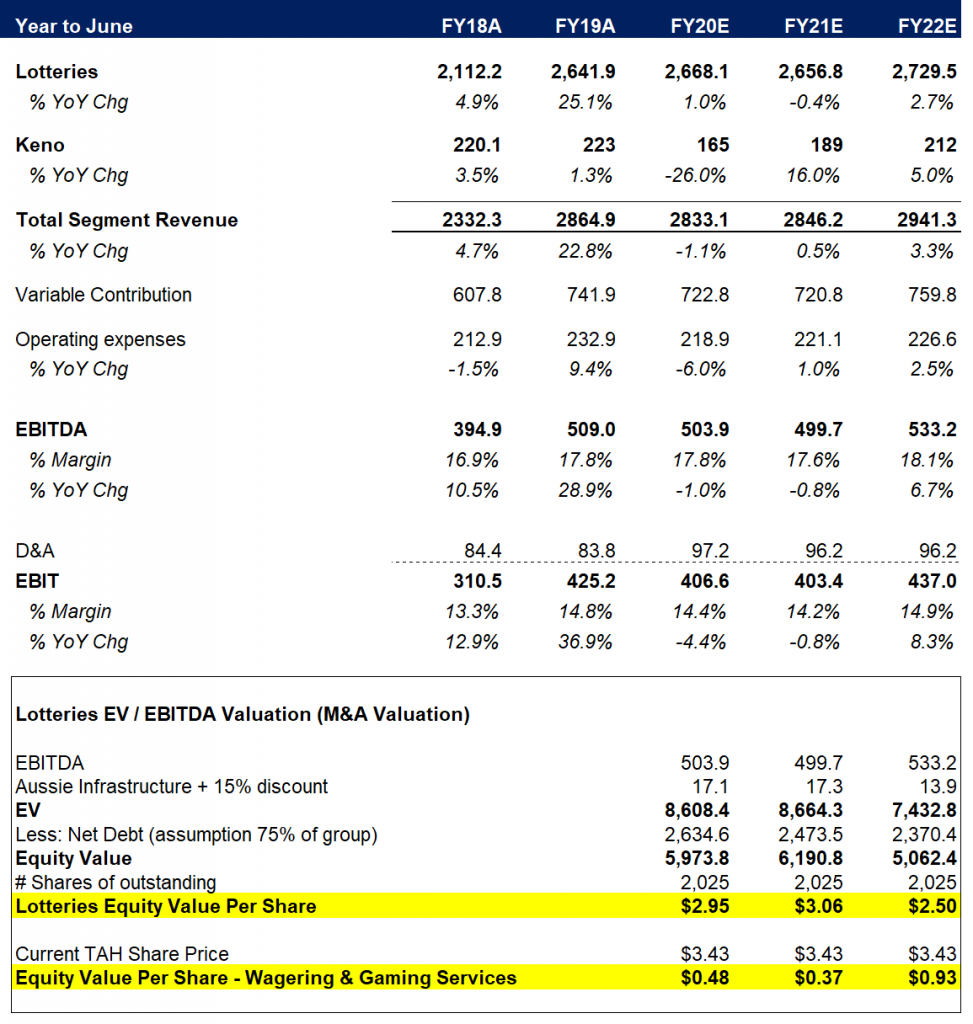

Earnings estimates and valuation. If we take management’s view on face value and ascribe a valuation multiple to the Lotteries business which is more in line with what the ASX-listed infrastructure assets are currently trading on, we come to the result highlighted in yellow in the figure below. Apart from our earnings assumptions for the segment (Lotteries and Keno business), our key assumptions are:

(1) Aussie peer group includes (SYD, TCL, AIA, AST, APA, ASX, AZJ, SKI – somewhat contentious given SYD / TCL tend to skew the multiples to the higher end) but applied a 15% discount as the Lotteries revenue can be lumpy due to the size of jackpots;

(2) Given the stability of earnings and long-dated licenses, we ascribe most of the group’s net debt to this segment.

Conclusion. The conclusion under these assumptions is that the current share price is ascribing very little value to the remaining TAH business (predominantly Wagering), despite its strong market position in Wagering (one could argue the challenges around competition in recent years is starting to recede). Or that if investors’ current valuation of TAH’s Wagering business is well north of $0.37 per share (highly possible), in that case they are significantly undervaluing the Lotteries business.

How can TAH monetise this mispricing? There has been suggestions TAH could look to spin out the Lotteries business, but frankly that seems very far off given they are only just getting through the merger with Tatts and subsequent synergies.

Management could look to introduce a capital partner to the Lotteries business (such as a pension fund) which could unlock capital and make the market ascribe a higher value to the business.

The point of the above exercise is to give clients another perspective on TAH. Not long ago some fund managers were calling out the Lotteries business as a “technology” play and therefore should be valued using the high multiples as the domestic tech sector. We have a Neutral view on the stock.

Find out more about BanyanTree Investment Group, their research, and portfolios by clicking here.

Investment Manager / Director at BanyanTree Investment Group

Latest posts by Zach Riaz (see all)

- Quick Update: Who bought the dip?Iron ore update + more - August 14, 2024

- What if we are NOT in a new “commodities supercycle”? - August 1, 2024

- Who is going to power the AI boom? - May 30, 2024

Leave a Comment

You must be logged in to post a comment.