Given recent developments in the Russia and Ukraine conflict, we thought it may be worthwhile providing clients historical context which may assist in how to think about the current situation. We remind clients that we highlighted in our recent Multi-Asset Quarterly published 2 Feb-22 that first half of CY22 was going to be volatile because of the U.S. Federal Reserve tightening cycle and the potential for the Russia / Ukraine conflict to “spiral out of control” – unfortunately appears to be playing out.

How much do geopolitical events impact stocks?

The short answer is, on average, not that much. Bloomberg collated data from 18 geopolitical events since 1940 which led to S&P 500 declines, which we have provided below. On average, the total drawdowns from these events was -5.4% and it takes approximately 15 days for the S&P 500 to bottom. The other key point to note from the table below is that the biggest drawdowns in S&P 500 took place in U.S. Terrorist Attacks, Iraq Invasion of Kuwait, North Korea Invades South Korea and Pearl Harbor Attack – which all resulted in the U.S. going to war.

With the U.S. just coming out of the debacle that was Afghanistan, we do not believe the U.S. has the appetite for another drawn out war. Further, from our understanding, U.S. President Joe Biden has ruled out sending troops to Ukraine. All else being equal, this geopolitical event does not concern us that much. In fact overnight all three U.S. indices – Dow Jones (+0.3%), S&P 500 (+1.5%) and NASDAQ Composite (+3.3%) – closed higher despite the invasion.

Mind you the early trading all indices saw very steep losses (that was the investors first reaction to the news) but investors over the course of the trading day clearly took the position that the Russia / Ukraine conflict will be brief. There was also big support for mega tech stocks – which probably drove the market higher.

Source: Bloomberg Intelligence

What does this mean for the U.S. Fed tightening cycle?

Whilst this is not the ideal situation in which the U.S. Fed wants to be raising rates in, we believe the U.S. Federal Reserve will still lift rates given the inflation numbers in the U.S. In fact, the Russia / Ukraine issue is further driving energy prices higher, which means a key contributor to the CPI number is likely to get worse or remain elevated in the short term. In fact overnight U.S. Fed officials have signaled as much, with some noting that the rate hike remains on track despite the Russia / Ukraine issue.

ECB unlikely to lift rates in CY22, in our view.

We noted in our most recent multi-asset quarterly reports that the Euro-zone economic growth could potentially disappoint expectations given “Restrictions in some parts of Europe remain and the ongoing threat of new Covid-19 variants will keep the possibility of economic growth exceeding expectations unlikely.” Now add to this the Russia & Ukraine conflict. In our view, the European Central Bank (ECB) could still go ahead with its plans to end the PEPP program (emergency program for ECB to buy a range of assets) in Mar-22, but is very much unlikely to raise interest rates along with the end of QE given recent developments. With the U.S. Fed still expected to move, this will result in yield divergence between the U.S. dollar and the euro.

Rising USD is a problem for the rest of the world.

The U.S. dollar (USD) was higher overnight following the Russia / Ukraine news, given its safe haven label. On the other side the Euro is much weaker over the past 3 days. As we have previously noted, the USD is a countercyclical currency, and a high USD is typically not positive for ex-U.S. equities. The recent increase in USD is likely tightening financial conditions around the globe already (key global commodities, contracts and debt servicing/coupons are priced in USD). This may have implications for global growth in our view. We could see the IMF downgrade global growth again this year given there will be some implications for global growth from the Russia / Ukraine conflict.

Rising oil prices are a concern for the broader market.

Unsurprisingly, oil prices jumped on the Russia / Ukraine conflict news but have settled lower. You can see in the chart below the WTI oil price breached the $100/bbl level but came off.

Source: Bloomberg

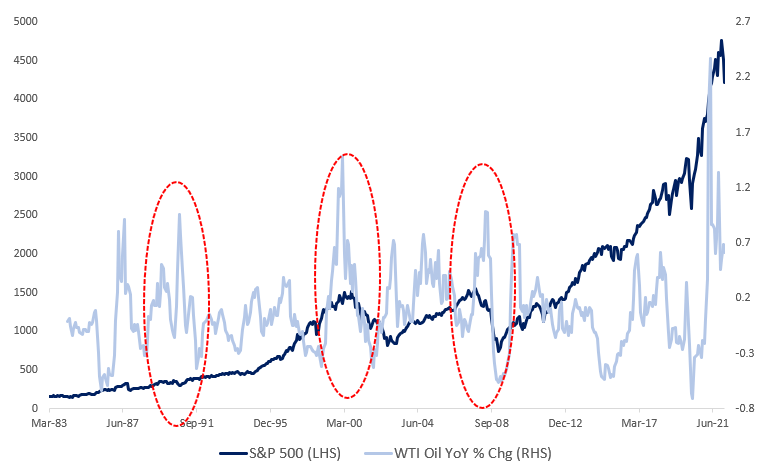

As highlighted in the chart below, in the past a significant jump in oil prices (as indicated by year-on-year % change) have preceded recessions in the U.S. and corrections in the S&P 500 Index. Further, a significantly higher oil price (say US$130 – 150 per barrel) will most certainly reduce global growth as well. However runaway oil prices are most certainly going to result in the U.S. putting pressure on Saudi Arabia to increase production. Saudi Arabia may push back and may instead enjoy the windfall from higher oil prices.

Source: Bloomberg, Banyantree

Our view

We are constantly discussing the developing macro and bottom up picture. But the team’s view, at this point, is still can we see good long-term buying opportunities in the current sell off.

Investment Manager / Director at BanyanTree Investment Group

Latest posts by Zach Riaz (see all)

- Quick Update: Who bought the dip?Iron ore update + more - August 14, 2024

- What if we are NOT in a new “commodities supercycle”? - August 1, 2024

- Who is going to power the AI boom? - May 30, 2024

Leave a Comment

You must be logged in to post a comment.